The Role of Firm Mergers in Innovation and Economic Growth

Insights from looking at competition policy from the perspective of dynamic competition

Mergers between firms and acquisitions of one firm by another are defining features of our modern economy. They shape how industries are organized and have a large influence on innovation and the nature of competition between firms. However, traditional competition policy has often taken a static view of market power and consumer welfare, potentially overlooking the long-term effects of mergers on economic growth and productivity.

Working with one of my former professors from my doctoral studies at the University of Minnesota, David M. Rahman, we are developing an endogenous growth model that incorporates novel dynamic competition processes to evaluate how horizontal mergers influence welfare through multiple dimensions.

Our modeling framework provides a different perspective on how merger policies should be designed to balance market concentration, innovation, and economic dynamism.

Understanding the Model: Mergers Beyond Market Power

Traditional economic analysis of mergers tends to focus on two main effects: increasing market power (which raises prices and reduces consumer welfare) and creating cost synergies (which reduces production costs). However, we propose a broader framework incorporating five key dimensions:

Market Power: Mergers reduce competition, leading to higher markups and potential deadweight losses.

Cost Synergies: Mergers may decrease operational costs, improving firm efficiency.

Innovation at the Extensive Margin: Higher expected profits encourage agents to invest more effort into new startups.

Innovation at the Intensive Margin: By changing the competitive landscape, mergers influence firms’ investments in productivity improvements.

Research Duplication: By reducing the number of competing firms, mergers reduce the duplication of research efforts, allocating resources for research more efficiently.

We are constructing and calibrating a dynamic general equilibrium model that accounts for these five factors. Our approach contrasts with typical merger guidelines, which often focus on static measures like the Herfindahl-Hirschman Index (HHI) to assess market concentration. However, this kind of approach has a long history in economics and anti-trust, with writers such as Schumpeter already arguing a century ago that what really matters for competition is not the level of markups but the dynamism of the economy.

How Mergers Shape Growth and Welfare

We calibrated the model using the US economy, and by simulating different merger policies, our model revealed several important insights about the trade-offs involved in regulating mergers.

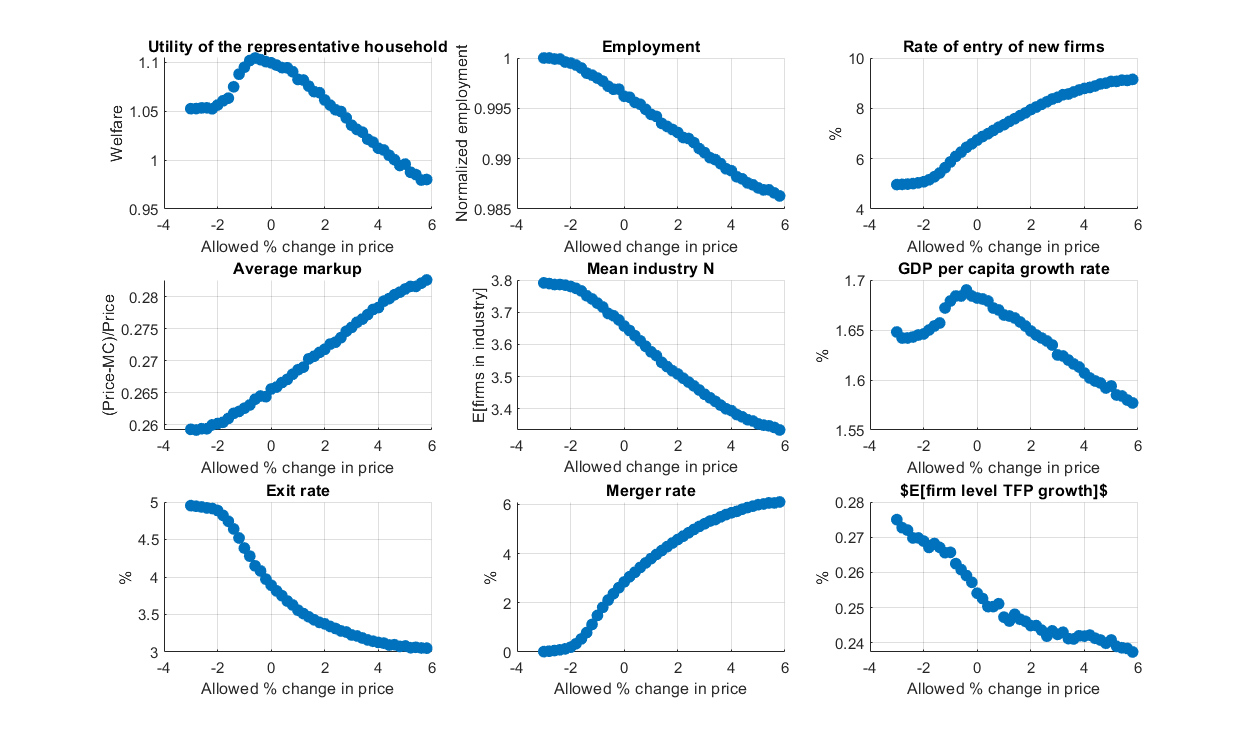

One policy that we have analyzed in detail is a simple rule that applies to the whole economy that authorizes mergers based on the projected change in price. Given this rule, the figure below shows several effects on the macroeconomic outcomes.

Note the considerable noise in some of our results as we ran our economy in a Monte Carlo simulation, approximating a theoretical model with a continuum of industries using a grid of only several thousand industries.

1. The Optimal Merger Policy Might be More Restrictive than the Current Status Quo in the US

One of the most striking results is that optimal merger policy is stricter than our calibration of current U.S. merger policy. While allowing all mergers would significantly hinder economic prosperity, blocking all mergers is also suboptimal. Instead, we found a carefully calibrated policy that maximizes welfare and, as a result, economic growth.

Our optimal merger policy leads to a GDP per capita growth rate of 1.69%—higher than the growth rate under existing policies: we find the first-order effect of merger policy is not on allocative efficiency but on the merger policy’s effects of macroeconomic growth dynamics. Indeed, according to our calibration, the GDP per capita growth rate varies by as much as 25% from the set of policies we considered. These include a policy of allowing any mergers (including the formation of monopolies), a policy of banning all mergers, and our candidate for the optimal policy: a policy of allowing mergers that change prices with a tolerance parameter calibrated to the degree of entry barriers in each industry.

According to the current version of our calibrated model, the best policies we found so far generate a situation where the rate at which firms merge is approximately 2.5% to 3% per year. Currently, it appears that US public firms merge at a rate of 3.8% to 4.5%, according to different sources.

2. Entry Barriers Matter More than Markups

A crucial takeaway is that merger policy should prioritize maintaining low entry barriers rather than solely focusing on keeping markups low. When entry barriers are low, even a lax merger policy does not harm long-term welfare because new firms can enter and discipline market power. However, when entry barriers are high, mergers can lead to long-lasting negative effects by stifling competition and innovation.

3. Price-Based Merger Rules Can Enhance Welfare

We evaluated different merger rules and found that a price-based policy—where mergers are allowed only if they do not increase industry prices beyond a certain threshold—outperforms concentration-based policies like HHI. The optimal price threshold in the model is -0.50%, meaning that mergers should be blocked if they are expected to raise prices by more than this amount.

However, we also found that if we consider a price-based merger policy that takes into account the degree of entry barriers in each industry, we can achieve even higher welfare than under this simple price rule for all industries in the economy while allowing substantially more mergers.

Policy Implications: Rethinking Competition Policy for Innovation-Driven Growth

The findings from our research have several important implications for policymakers:

Shift the Focus from Market Concentration to Entry Barriers: The study suggests that regulators should focus on fostering an environment where new firms can enter and compete rather than merely limiting firm size through HHI-based rules.

Incorporate Dynamic Considerations into Merger Guidelines: Static models that focus on immediate price effects may underestimate the long-term consequences of mergers on innovation and productivity growth.

Use Price-Based Rules for Merger Approvals: The research supports the idea that a price increase threshold is a more effective criterion for assessing mergers than concentration-based metrics.

Encourage Policies that Reduce Unnecessary Research Duplication: By recognizing that mergers can sometimes prevent inefficient duplication of research efforts, policymakers should balance their approach rather than outright discouraging consolidation.

We have reached the conclusion that policymakers should adapt their approach to competition policy to ensure that it also fosters productivity growth through innovation instead of focusing mostly on static misallocation effects. Although these static effects are still significant, we are finding that their effects on welfare are smaller than the dynamic effects of competition policy.